Mastering 2026 Tax Changes: Your Guide to Maximizing Deductions

The landscape of taxation is constantly evolving, and as we approach 2026, significant changes are on the horizon that could profoundly impact your financial planning. Understanding these shifts, particularly concerning 2026 tax deductions, is not just about compliance; it’s about strategic financial optimization. The upcoming tax season, culminating in the April 15th deadline, will require a proactive approach to ensure you are maximizing every available opportunity to reduce your taxable income. This comprehensive guide aims to demystify the impending tax code revisions, providing you with actionable insights and practical strategies to navigate the complexities and make the most of your deductions.

The year 2026 marks a crucial juncture for many taxpayers. Several provisions from the Tax Cuts and Jobs Act (TCJA) of 2017 are set to expire or change, which could lead to substantial alterations in individual income tax rates, standard deductions, and various itemized deductions. For both individuals and businesses, these adjustments mean that what worked in previous tax years might not be the most effective strategy moving forward. Staying informed and adapting your financial habits now can save you significant amounts of money and stress in the future. Our focus here is to arm you with the knowledge to prepare effectively, ensuring you’re not caught off guard by the new rules.

From understanding the nuances of the standard deduction versus itemized deductions to exploring new credits and deductions that might become available, this article will cover the essential aspects you need to know. We’ll delve into specific areas such as changes to personal exemptions, modifications to the child tax credit, and potential impacts on state and local tax (SALT) deductions. Furthermore, we’ll provide practical tips for record-keeping, professional consultation, and proactive planning to help you secure your financial well-being under the new tax regime. The goal is to transform potential challenges into opportunities for greater financial efficiency and savings. Let’s embark on this journey to master your 2026 tax deductions.

The Evolving Tax Landscape: What’s Changing in 2026?

The year 2026 is poised to bring some of the most significant tax code changes in recent memory, primarily due to the sunsetting provisions of the Tax Cuts and Jobs Act (TCJA) of 2017. When the TCJA was enacted, many of its individual tax provisions were designed with an expiration date of December 31, 2025. This means that starting January 1, 2026, without further legislative action, we will revert to many of the tax laws that were in place prior to 2018. Understanding these core changes is the first step in preparing to maximize your 2026 tax deductions.

Individual Income Tax Rates and Brackets

One of the most impactful changes will be to individual income tax rates and brackets. The TCJA lowered tax rates across most income brackets. Come 2026, these rates are expected to increase for many taxpayers, reverting to pre-TCJA levels. For example, the current 10%, 12%, 22%, 24%, 32%, 35%, and 37% brackets could shift back to 10%, 15%, 25%, 28%, 33%, 35%, and 39.6%. This means that without careful planning, more of your income could be subject to higher taxation. It’s crucial to review your income projections and understand how these potential rate increases will affect your overall tax liability. This could influence decisions on income deferral or acceleration strategies.

Standard Deduction Amounts

The TCJA significantly increased the standard deduction, leading many taxpayers to opt for it instead of itemizing. In 2026, the standard deduction amounts are scheduled to decrease, reverting to their pre-TCJA levels, adjusted for inflation. While still a substantial deduction, the reduced amount might push more taxpayers back into itemizing their deductions if their eligible itemized expenses exceed the new standard deduction threshold. This change alone will require a fresh evaluation of whether to itemize or take the standard deduction, making understanding your potential 2026 tax deductions even more critical.

Personal Exemptions Reinstatement

Under the TCJA, personal exemptions were eliminated. Prior to 2018, taxpayers could claim a personal exemption for themselves, their spouse, and each dependent, which effectively reduced their taxable income. In 2026, personal exemptions are expected to be reinstated, again adjusted for inflation. While this will provide a direct reduction in taxable income for many, its impact must be considered alongside the changes to the standard deduction and other credits. For larger families, the return of personal exemptions could be quite beneficial.

Child Tax Credit Modifications

The TCJA expanded the Child Tax Credit (CTC) to $2,000 per qualifying child, with a significant portion being refundable. In 2026, the CTC is set to revert to its pre-TCJA amount of $1,000 per qualifying child, and the refundable portion may also be reduced or subject to stricter limitations. This change will have a considerable impact on families with children, potentially increasing their tax liability. Understanding the new rules for the CTC will be essential for family tax planning and maximizing available 2026 tax deductions and credits.

State and Local Tax (SALT) Deduction Cap

The TCJA introduced a $10,000 cap on the deduction for state and local taxes (SALT), which has been a contentious issue, particularly for residents in high-tax states. This cap is also scheduled to expire at the end of 2025. If the cap is lifted, taxpayers in high-SALT states could see a significant increase in their itemized deductions, potentially leading to a lower overall tax burden. However, the political debate around the SALT cap is ongoing, and its future remains somewhat uncertain. Staying abreast of legislative developments will be key here.

Other Itemized Deductions

Many other itemized deductions that were eliminated or limited by the TCJA are also slated to return or change. These could include miscellaneous itemized deductions subject to the 2% adjusted gross income (AGI) floor, such as unreimbursed employee business expenses, tax preparation fees, and investment expenses. While these might not affect every taxpayer, those with significant professional or investment-related expenses should pay close attention to their potential reinstatement. The return of these deductions could offer new avenues for reducing taxable income.

In summary, the 2026 tax year promises a substantial overhaul of the individual tax code. These changes necessitate a thorough review of your current financial strategies and a proactive approach to planning. By understanding these shifts well in advance, you can position yourself to effectively navigate the new tax environment and make informed decisions regarding your 2026 tax deductions.

Maximizing Your 2026 Tax Deductions: Proactive Strategies

With the impending changes to the tax code in 2026, a proactive approach to financial planning is more crucial than ever. Simply reacting to the new rules once they are in effect could mean missing out on valuable opportunities to maximize your 2026 tax deductions. This section will outline key strategies you can implement now and continue through 2026 to optimize your tax position.

Re-evaluating Standard vs. Itemized Deductions

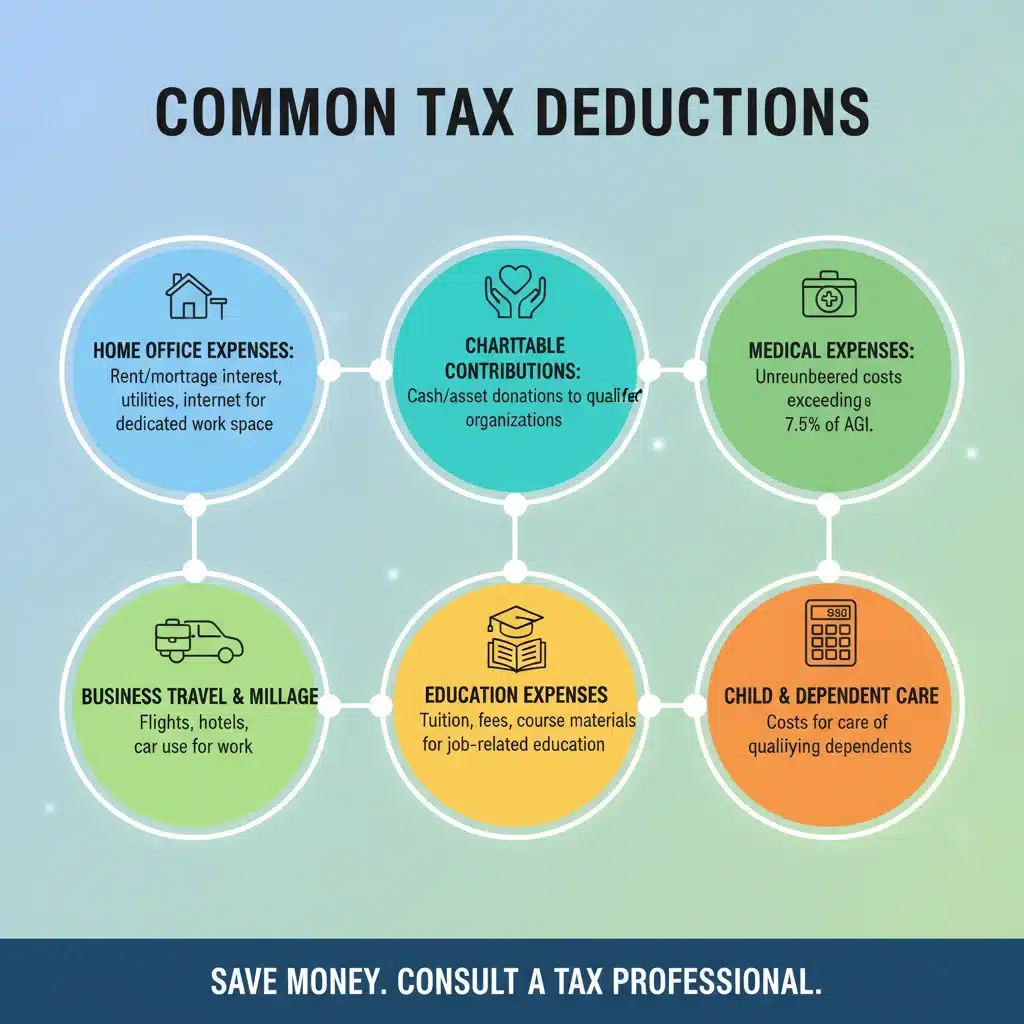

As the standard deduction amounts are expected to decrease, and personal exemptions are set to return, it’s imperative to re-evaluate whether itemizing will be more beneficial for you in 2026. Start by tracking all potential itemized deductions meticulously. These typically include:

- Mortgage Interest: Keep records of all interest paid on your home mortgage.

- State and Local Taxes (SALT): If the cap is lifted, this could be a significant deduction. Continue to track your property taxes, state income taxes, or sales taxes.

- Charitable Contributions: Maintain detailed records of all cash and non-cash donations to qualified charities. Consider ‘bunching’ deductions, where you accelerate several years’ worth of charitable giving into one year to exceed the standard deduction threshold.

- Medical Expenses: If your unreimbursed medical expenses exceed a certain percentage of your Adjusted Gross Income (AGI), they can be deductible. Keep track of all doctor visits, prescription costs, insurance premiums, and other medical outlays.

- Other Potential Deductions: Be aware of the possible return of miscellaneous itemized deductions, such as unreimbursed employee business expenses or tax preparation fees.

By keeping a detailed ledger of these expenses, you can make an informed decision when it’s time to file, ensuring you choose the option that yields the greatest tax savings.

Strategic Charitable Giving

Charitable contributions remain a powerful tool for maximizing 2026 tax deductions. Beyond direct cash donations, consider these strategies:

- Donor-Advised Funds (DAFs): A DAF allows you to make a charitable contribution, receive an immediate tax deduction, and then recommend grants to your favorite charities over time. This is an excellent way to ‘bunch’ deductions.

- Qualified Charitable Distributions (QCDs): If you are 70.5 or older and have an IRA, you can make a QCD directly from your IRA to a qualified charity. This distribution counts towards your Required Minimum Distribution (RMD) and is not included in your gross income, offering a tax-efficient way to give.

- Appreciated Securities: Donating appreciated stocks or mutual funds held for more than one year can provide a double tax benefit. You can deduct the fair market value of the securities and avoid paying capital gains tax on the appreciation.

Optimizing Retirement Contributions

Contributing to retirement accounts like 401(k)s and IRAs is one of the most effective ways to reduce your taxable income and boost your 2026 tax deductions. Contributions to traditional 401(k)s and IRAs are typically tax-deductible in the year they are made, reducing your current year’s taxable income. Maximize these contributions to the extent possible, especially if you anticipate being in a higher tax bracket in 2026 due to the rate changes. Remember to factor in catch-up contributions if you are age 50 or older.

Health Savings Accounts (HSAs)

If you are eligible for a Health Savings Account (HSA) through a high-deductible health plan, take full advantage of it. HSAs offer a triple tax advantage:

- Contributions are tax-deductible (or pre-tax if made through payroll).

- Earnings grow tax-free.

- Qualified withdrawals for medical expenses are tax-free.

HSAs are often referred to as ‘super IRAs’ due to their unparalleled tax benefits, making them an excellent tool for increasing your 2026 tax deductions and saving for future medical costs.

Education-Related Deductions and Credits

For those with education expenses, be mindful of potential deductions and credits. While some credits have income limitations, they can significantly reduce your tax liability. The American Opportunity Tax Credit and the Lifetime Learning Credit are two prominent examples. Additionally, deductions for student loan interest and tuition and fees (if reinstated or modified) can help lower your taxable income. Keep meticulous records of all education-related expenses.

Business Expense Deductions (for Self-Employed/Small Businesses)

If you are self-employed or own a small business, understanding and claiming all eligible business expenses is paramount. The TCJA made some changes to business deductions, but many core deductions remain. These can include:

- Home office expenses (if you meet the strict criteria).

- Business travel, meals, and entertainment (subject to limits).

- Vehicle expenses.

- Professional development and education.

- Health insurance premiums (if self-employed).

- Contributions to self-employed retirement plans (SEP IRA, Solo 401(k)).

It’s crucial to separate personal and business expenses and maintain diligent records to substantiate all claims. Consulting with a tax professional specializing in small business taxation can help ensure you are maximizing all available 2026 tax deductions.

Tax Loss Harvesting

Consider tax loss harvesting in your investment portfolio. This strategy involves selling investments at a loss to offset capital gains and potentially up to $3,000 of ordinary income. If you have significant capital gains, this can be an effective way to reduce your overall tax burden. While this is an ongoing strategy, it becomes even more relevant if capital gains tax rates are also subject to change in 2026.

Reviewing Your Withholding

As tax rates and deductions change, your tax withholding might need adjustment. Use the IRS Tax Withholding Estimator tool to ensure you are not over-withholding (giving the government an interest-free loan) or under-withholding (potentially facing penalties). Adjusting your W-4 proactively can help manage your cash flow throughout the year and prevent surprises when filing your 2026 tax deductions.

By implementing these proactive strategies, you can position yourself to effectively navigate the 2026 tax code changes and ensure you are maximizing every available deduction and credit. Early planning and diligent record-keeping are your best allies in this endeavor.

Understanding the April 15th Deadline: Beyond Just Filing

The April 15th deadline (or the next business day if the 15th falls on a weekend or holiday) is synonymous with tax filing, but its significance extends beyond merely submitting your tax return. For 2026, with the anticipated tax code changes, understanding the implications of this deadline for your 2026 tax deductions and overall financial strategy becomes even more critical. It’s a culmination of a year’s worth of financial decisions and a gateway to the next fiscal period.

Filing Your Return and Paying Taxes Due

The most obvious aspect of the April 15th deadline is the requirement to file your federal income tax return and pay any taxes owed. Failure to file or pay on time can result in penalties and interest. With potential changes to tax rates and deductions, it’s possible that more taxpayers might owe money or see a different refund amount than in previous years. Therefore, accurate preparation is paramount. Utilize tax software or a tax professional to ensure your return is correct and filed promptly.

Making Estimated Tax Payments

For self-employed individuals, freelancers, and those with significant income not subject to withholding, April 15th is also the deadline for the first quarterly estimated tax payment for the current tax year. The changes to tax rates and potentially the reinstatement of certain deductions will impact how you calculate these estimated payments. It’s crucial to adjust your estimates to avoid underpayment penalties. The IRS provides Form 1040-ES for calculating and making these payments. The other quarterly deadlines are June 15th, September 15th, and January 15th of the following year.

Contributing to Retirement Accounts

April 15th is often the last day to contribute to an IRA or HSA for the previous tax year. This means you have until this deadline to make contributions that can reduce your taxable income for the tax year just ended. For example, for your 2025 tax return (filed by April 15, 2026), you can still make IRA or HSA contributions up to the deadline. This is a powerful, last-minute opportunity to maximize your 2026 tax deductions and savings.

Filing for an Extension

If you need more time to prepare your tax return, you can file for an extension using Form 4868. This typically grants you an additional six months to file, pushing your deadline to October 15th. However, it’s crucial to remember that an extension to file is NOT an extension to pay. If you expect to owe taxes, you must estimate and pay that amount by April 15th to avoid penalties and interest. Filing an extension can be a wise move if you have complex financial situations or are awaiting crucial tax documents.

Reviewing Your Tax Situation for the Upcoming Year

The April 15th deadline should also serve as a prompt to review your tax situation for the *upcoming* year. The changes set for 2026 mean that what you filed in April 2026 (for the 2025 tax year) might not accurately reflect your tax obligations for the 2026 tax year. Use this time to:

- Adjust Withholding: Re-evaluate your W-4 form with your employer to ensure your withholding accurately reflects the new tax rates and your anticipated 2026 tax deductions.

- Update Estimated Payments: If you make estimated payments, revise your calculations for the 2026 tax year to account for the new rules.

- Revisit Financial Goals: Align your financial goals with the new tax environment. Are there new investment opportunities or savings strategies that become more attractive?

Record-Keeping and Documentation

Effective tax planning and maximizing 2026 tax deductions heavily rely on meticulous record-keeping. The April 15th deadline highlights the importance of having all your documentation in order. This includes:

- Income statements (W-2s, 1099s).

- Records of deductions (receipts for charitable donations, medical expenses, business expenses).

- Investment statements.

- Property tax statements.

- Any other relevant financial documents.

Organizing these documents throughout the year, rather than scrambling at tax time, will save you time and help ensure you don’t miss any eligible deductions.

Consulting with a Tax Professional

Given the complexity of the upcoming tax code changes, consulting with a qualified tax professional is highly recommended. They can provide personalized advice, help you understand how the 2026 changes specifically impact your financial situation, and assist in identifying all eligible 2026 tax deductions. A professional can also help you with long-term tax planning strategies to optimize your financial health under the new regulations.

In essence, the April 15th deadline for 2026 is more than just a due date; it’s a critical checkpoint for financial readiness. By understanding its various facets and taking proactive steps, you can navigate the new tax environment with confidence and maximize your financial outcomes.

Key Areas for Business Tax Deductions in 2026

While much of the discussion around 2026 tax changes focuses on individual taxpayers, businesses, particularly small and medium-sized enterprises (SMEs), will also face significant adjustments. Understanding these changes and how to leverage business-specific 2026 tax deductions is vital for maintaining profitability and ensuring compliance. The expiration of certain TCJA provisions will reshape the corporate tax landscape and impact how businesses operate and plan their finances.

Section 179 Expensing and Bonus Depreciation

The TCJA significantly enhanced Section 179 expensing and introduced 100% bonus depreciation, allowing businesses to immediately deduct the full cost of eligible new and used assets placed in service. While Section 179 is permanent, the 100% bonus depreciation is scheduled to phase out, dropping to 80% in 2023, 60% in 2024, 40% in 2025, and 20% in 2026, before being eliminated in 2027. This gradual reduction means businesses need to strategically plan their capital expenditures. Accelerating significant purchases into 2025 could allow for higher bonus depreciation deductions, while careful planning will be needed for acquisitions in 2026 to maximize the remaining 20%.

Qualified Business Income (QBI) Deduction (Section 199A)

The Section 199A deduction, also known as the Qualified Business Income (QBI) deduction, allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income. This deduction is also set to expire at the end of 2025. Without legislative action, this valuable deduction will no longer be available in 2026. This potential loss will significantly impact the taxable income of many pass-through entities (S-corps, partnerships, sole proprietorships). Businesses should model their financial projections with and without this deduction to understand the potential increase in their tax liability and explore other strategies to mitigate it.

Net Operating Loss (NOL) Rules

The TCJA made significant changes to Net Operating Loss (NOL) rules, generally limiting the deduction to 80% of taxable income and eliminating NOL carrybacks for most businesses. Post-2025, these rules could revert to pre-TCJA provisions, potentially allowing for 100% of taxable income to be offset by NOLs and possibly reinstating carryback provisions. Businesses with fluctuating income or those anticipating losses in the near future should monitor these rules closely, as they can significantly impact liquidity and future tax planning.

Business Interest Expense Limitation (Section 163(j))

The TCJA limited the deduction for business interest expense to 30% of adjusted taxable income (ATI). For tax years beginning in 2022, the calculation of ATI changed, making the limitation more restrictive for many businesses. This limitation is permanent, but businesses should continue to monitor their interest expenses and how they interact with their ATI. Strategic debt management and understanding the nuances of this limitation will be key for maximizing 2026 tax deductions related to financing costs.

Research and Development (R&D) Expensing

Another significant change that began in 2022 and will continue into 2026 is the requirement to amortize (capitalize and deduct over time) R&D expenses rather than immediately deducting them. This change has a substantial impact on businesses that invest heavily in R&D, as it delays their ability to recognize these expenses for tax purposes. Businesses should adjust their cash flow forecasts and tax planning to account for this change, as it can reduce their immediate tax benefits, even if they are still eligible for other 2026 tax deductions.

Employee Benefits and Fringe Benefits

The tax treatment of various employee benefits and fringe benefits could also see adjustments. While some benefits remain tax-free to employees and deductible for employers, others might be subject to new limitations or requirements. Businesses should review their employee benefits packages to ensure they are structured in a tax-efficient manner for both the company and its employees. This includes understanding the deductibility of health insurance premiums, retirement plan contributions, and other perks.

Accounting Methods and Inventory Valuations

Businesses may also need to review their accounting methods and inventory valuation techniques in light of the evolving tax code. Changes in revenue recognition, inventory capitalization rules, or other accounting provisions could impact taxable income and require adjustments to financial reporting. Consulting with an accountant to ensure your business is using the most advantageous and compliant accounting methods for 2026 is a smart move.

Proactive Business Planning

For businesses, proactive planning is paramount. This includes:

- Forecasting: Develop detailed financial forecasts that account for potential changes in tax rates, deductions, and credits.

- Capital Expenditure Planning: Strategically time large purchases to maximize bonus depreciation or Section 179 expensing before their phase-out or elimination.

- Entity Structure Review: Re-evaluate your business entity structure (e.g., sole proprietorship, S-corp, C-corp) to ensure it remains the most tax-efficient option under the new rules.

- Professional Guidance: Engage with tax attorneys and CPAs who specialize in business taxation to navigate the complexities and identify all eligible 2026 tax deductions.

By staying informed and taking proactive steps, businesses can mitigate potential negative impacts of the 2026 tax code changes and continue to thrive in the evolving economic environment.

The Importance of Professional Guidance for 2026 Tax Deductions

Navigating the complex and shifting landscape of tax law, especially with the significant changes anticipated in 2026, can be daunting. While this guide provides a comprehensive overview, the nuances of individual and business financial situations often require personalized expertise. This is where the importance of professional guidance comes into play, particularly when it comes to maximizing your 2026 tax deductions.

Personalized Tax Planning

Every taxpayer’s financial situation is unique. What works for one might not be ideal for another. A qualified tax professional – such as a Certified Public Accountant (CPA), an Enrolled Agent (EA), or a tax attorney – can provide personalized advice tailored to your specific income, expenses, investments, and family situation. They can help you understand how the 2026 tax code changes will individually impact you and identify the most effective strategies for your circumstances. This bespoke planning is invaluable for optimizing your 2026 tax deductions.

Understanding the Nuances of New Regulations

Tax laws are not always straightforward. The language can be intricate, and the implementation of new provisions often comes with specific rules, exceptions, and interpretations. Tax professionals spend their careers studying these complexities. They can help you correctly interpret the new regulations, such as the reinstatement of personal exemptions, changes to the Child Tax Credit, or the potential lifting of the SALT cap. Their expertise ensures you don’t misinterpret a rule and inadvertently miss out on a deduction or, worse, face penalties.

Identifying All Eligible Deductions and Credits

With the potential return of various itemized deductions and changes to existing ones, it can be challenging for the average taxpayer to identify every single deduction or credit they are eligible for. A professional will have an in-depth knowledge of all available 2026 tax deductions and credits, including those that are often overlooked. They can review your financial records with a keen eye, ensuring that no stone is left unturned in your quest to reduce your taxable income.

Strategic Tax Optimization

Beyond simply filling out forms, tax professionals engage in strategic tax optimization. This involves looking at your financial picture holistically and recommending actions that can reduce your tax burden not just for the current year, but also for future years. This might include advice on:

- Income deferral or acceleration.

- Investment strategies that are tax-efficient.

- Optimal timing for charitable contributions.

- Structuring business transactions for maximum tax benefit.

- Estate planning considerations in light of tax law changes.

Such foresight is critical in a changing tax environment and can lead to substantial long-term savings.

Audit Support and Representation

While no one hopes for an audit, it’s a possibility. Having a tax professional prepare your return and provide advice can significantly reduce the likelihood of an audit. If you do face an IRS inquiry or audit, a professional can represent you, communicate with the tax authorities on your behalf, and help you navigate the process, providing peace of mind and potentially a more favorable outcome. Their expertise in substantiating 2026 tax deductions and other claims is invaluable.

Saving Time and Reducing Stress

Preparing taxes, especially with upcoming changes, can be time-consuming and stressful. Delegating this task to a professional frees up your time and reduces anxiety, allowing you to focus on other aspects of your life or business. Knowing that your taxes are being handled by an expert provides confidence that your return is accurate, compliant, and optimized for your financial benefit.

Staying Current with Legislative Developments

Tax laws are not static. While 2026 brings scheduled changes, there’s always the possibility of further legislative action. Tax professionals stay current with these developments, ensuring that their advice and your tax planning remain up-to-date. This ongoing vigilance is crucial for adapting to any last-minute adjustments or new opportunities related to 2026 tax deductions.

In conclusion, while self-preparation tools are available, the complexity of the 2026 tax code changes makes professional guidance an investment rather than an expense. It can lead to significant savings, reduce risk, and provide invaluable peace of mind, ensuring you are fully prepared for the April 15th deadline and beyond.

Conclusion: Preparing for Your Best Tax Outcome in 2026

The journey through the intricate world of taxation, especially with the anticipated shifts in 2026, can seem daunting. However, by understanding the core changes and adopting a proactive approach, you can transform potential challenges into significant opportunities for financial optimization. This comprehensive guide has aimed to equip you with the knowledge and strategies necessary to navigate the evolving tax landscape and maximize your 2026 tax deductions.

We’ve explored the significant sunsetting provisions of the Tax Cuts and Jobs Act (TCJA) of 2017, highlighting key areas such as individual income tax rates, standard deduction amounts, the reinstatement of personal exemptions, and modifications to the Child Tax Credit. We also touched upon the critical, ongoing debate surrounding the State and Local Tax (SALT) deduction cap and the potential return of various miscellaneous itemized deductions. For businesses, the phase-out of bonus depreciation, the expiration of the Section 199A QBI deduction, and changes to R&D expensing are paramount considerations.

The core message remains clear: early preparation and diligent record-keeping are your most powerful allies. Begin now to track all potential deductions, whether personal expenses like medical costs and charitable contributions, or business-related outlays. Re-evaluate your financial strategies, from retirement contributions and HSA utilization to strategic charitable giving and investment planning. Consider ‘bunching’ deductions or timing capital expenditures to take advantage of current rules before they change.

Furthermore, the April 15th deadline for 2026 is not merely a filing date; it’s a critical checkpoint for assessing your previous year’s financial performance and planning for the year ahead. Use this time to adjust your withholdings, update estimated tax payments, and align your financial goals with the new tax environment. Remember that making timely contributions to retirement accounts and HSAs can still provide valuable last-minute deductions for the preceding tax year.

Perhaps most importantly, do not underestimate the value of professional guidance. A qualified tax professional can offer personalized advice, help you interpret complex regulations, identify every eligible 2026 tax deduction, and provide strategic optimization for your unique financial situation. Their expertise can save you time, reduce stress, and ultimately lead to a more favorable tax outcome and greater financial peace of mind.

As 2026 approaches, the tax code will undoubtedly present new complexities. However, by staying informed, planning proactively, and seeking expert advice, you can confidently navigate these changes. Your diligence today will pave the way for a more efficient and beneficial tax season, ensuring you maximize every opportunity to reduce your tax liability and secure your financial future. Start planning now, and make the 2026 tax year your most financially optimized one yet.