Mastering Student Loan Repayment: New Programs for 2026 Graduates

The looming shadow of student loan debt is a stark reality for millions of graduates, and for the class of 2026, understanding the landscape of repayment options is more critical than ever. As the economy evolves and policy makers strive to address the student debt crisis, new programs and initiatives are continuously being introduced. For those graduating in 2026, a proactive approach to understanding these options can mean the difference between financial freedom and years of struggle. This comprehensive guide will delve into three pivotal new programs specifically designed to assist 2026 graduates with their student loan repayment, offering practical solutions and highlighting their potential financial impact. Our goal is to equip you with the knowledge to make informed decisions, navigate the complexities of student loan repayment 2026, and ultimately, achieve financial stability.

Navigating the Post-Graduation Financial Landscape: Why Understanding Student Loan Repayment 2026 is Key

Graduating college is a monumental achievement, a culmination of years of hard work, dedication, and often, significant financial investment. For many, this investment comes in the form of student loans, which, while enabling access to education, also bring a substantial financial obligation. The class of 2026 is entering a unique economic environment, shaped by global events, technological advancements, and evolving job markets. Consequently, the strategies for managing student loan repayment 2026 are not static; they are dynamic and require continuous attention and adaptation.

The sheer volume of student debt in the United States is staggering, exceeding trillions of dollars. This national challenge has spurred various legislative and administrative efforts to provide relief and streamline repayment processes. As a 2026 graduate, you are positioned to benefit from or be impacted by these changes. Ignoring your student loan obligations or failing to explore available programs can lead to missed opportunities for lower payments, interest subsidies, or even loan forgiveness. Therefore, a deep dive into the specifics of student loan repayment 2026 is not just advisable, but essential for your long-term financial health.

It’s not just about making payments; it’s about making smart payments. This involves understanding your loan types (federal vs. private), interest rates, repayment terms, and crucially, the eligibility criteria for various assistance programs. The landscape of student loan repayment 2026 is designed to offer a lifeline, but only if you know where to look and how to apply. This article will serve as your compass, guiding you through the newest and most impactful programs that can significantly alleviate your post-graduation financial burden.

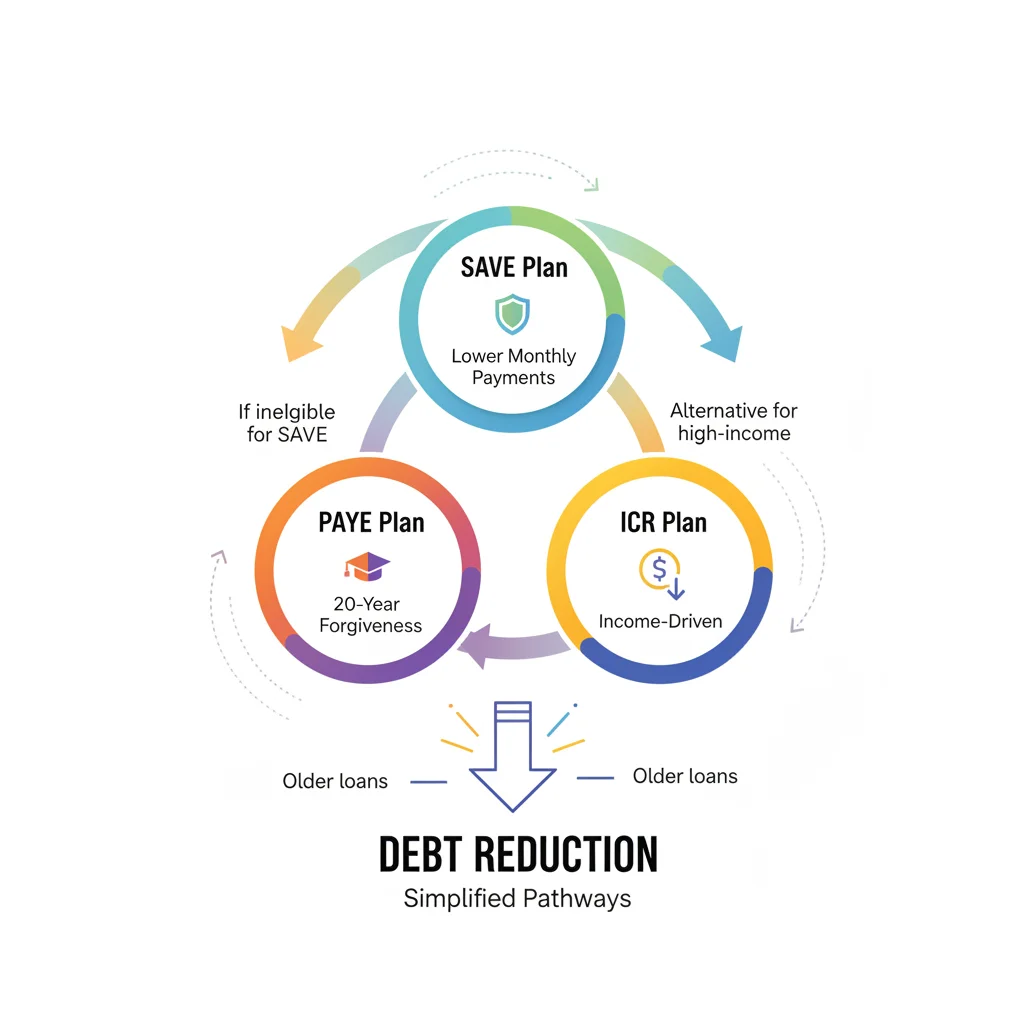

Program 1: The Enhanced Income-Driven Repayment (IDR) Plan for 2026 Graduates

One of the most significant evolutions in student loan repayment has been the continuous refinement of Income-Driven Repayment (IDR) plans. For 2026 graduates, a newly enhanced IDR plan is set to offer unprecedented flexibility and relief. This program builds upon existing IDR frameworks but introduces several key modifications designed to make payments more affordable and accelerate the path to forgiveness.

Key Features and Benefits:

- Lower Discretionary Income Calculation: The new IDR plan redefines ‘discretionary income,’ increasing the amount of income protected from repayment calculations. This means a larger portion of your income will be excluded when determining your monthly payment, leading to significantly lower payments for many borrowers. For example, instead of 150% of the poverty line, it might protect 225%, leaving less income subject to the repayment formula. This adjustment is a game-changer for those struggling with high cost-of-living expenses right out of college.

- Reduced Payment Percentage: Under previous IDR plans, payments were typically set at 10% of your discretionary income. This enhanced plan lowers that percentage, potentially to 5% or even less for undergraduate loans. This reduction directly translates to smaller monthly outflows, freeing up funds for other essential expenses or savings. This is a direct, tangible benefit for managing student loan repayment 2026.

- Faster Forgiveness for Lower Balances: A groundbreaking feature of this enhanced IDR plan is the introduction of accelerated forgiveness for borrowers with smaller loan balances. While traditional IDR plans require 20 or 25 years of payments for forgiveness, this new provision could allow borrowers with original balances below a certain threshold (e.g., $12,000) to receive forgiveness after as little as 10 years of payments. This incentivizes prompt, consistent payments and offers a quicker path to being debt-free for a substantial segment of 2026 graduates.

- Interest Subsidy: A common frustration with IDR plans is that interest can accrue even when making payments, sometimes leading to a growing loan balance despite consistent effort. The enhanced IDR plan includes a provision where the government covers unpaid interest each month, preventing your loan balance from growing as long as you make your required (even if zero-dollar) payments. This eliminates the ‘negative amortization’ problem and makes IDR a much more effective tool for student loan repayment 2026.

Who Benefits Most?

This enhanced IDR plan is particularly beneficial for 2026 graduates who anticipate starting their careers with moderate incomes, those in public service roles, or individuals pursuing further education. It provides a crucial safety net, ensuring that your student loan payments are manageable regardless of your starting salary. It also offers a clear pathway to forgiveness, reducing the long-term burden of debt.

Actionable Steps:

- Understand Your Loan Types: Confirm if your federal loans are eligible for IDR. Most Direct Loans and some FFEL Program loans are.

- Gather Financial Documents: You’ll need your most recent tax return or other proof of income to apply.

- Apply Annually: IDR plans require annual reapplication to update your income and family size. Mark your calendar!

- Utilize the Loan Simulator: The Department of Education’s Loan Simulator tool can help you compare this new IDR plan with other options to see which offers the lowest monthly payment and total cost. This is a vital step in optimizing your student loan repayment 2026 strategy.

Program 2: The Public Service Loan Forgiveness (PSLF) Expansion and Simplification

The Public Service Loan Forgiveness (PSLF) program has long been a beacon of hope for graduates entering public service careers. However, its complex rules and high denial rates have historically frustrated many eligible borrowers. For 2026 graduates, significant expansions and simplifications are being implemented to make PSLF more accessible and reliable, truly fulfilling its promise of debt relief for those dedicated to serving their communities.

Key Enhancements:

- Broader Employer Eligibility: The definition of ‘qualifying employer’ is being clarified and potentially expanded to include a wider range of non-profit organizations and government entities, including some that may have been previously excluded due to technicalities. This means more 2026 graduates working in vital public service roles will find their employment eligible for PSLF.

- Simplified Payment Tracking and Certification: One of the biggest hurdles for PSLF has been accurately tracking qualifying payments and employer certifications. New systems and processes are being implemented to streamline this. This could include automated tracking of eligible payments and easier digital submission of employer certification forms, significantly reducing the administrative burden and risk of error for borrowers. This simplification is crucial for successful student loan repayment 2026.

- Credit for Past Payments (Limited Lookback): While primarily for future payments, there’s discussion and potential for a limited ‘lookback’ period for certain past payments that might not have previously qualified but occurred while working for an eligible employer. While details are still being finalized, this could offer relief to some who previously thought they were ineligible. For 2026 graduates, this sets a precedent for clear, retroactive eligibility if rules change again in the future.

- Clearer Communication and Guidance: A major focus of the PSLF overhaul is improved communication from loan servicers and the Department of Education. This means clearer instructions, more accessible resources, and proactive outreach to ensure borrowers understand their eligibility and how to remain on track for forgiveness.

Who Benefits Most?

This expanded PSLF program is a game-changer for 2026 graduates pursuing careers in government (federal, state, local, tribal), non-profit organizations (501(c)(3) and others), public education, healthcare, social work, and other public service sectors. It offers a powerful incentive for these vital professions by providing a clear path to complete federal student loan forgiveness after 120 qualifying monthly payments.

Actionable Steps:

- Confirm Employer Eligibility: As soon as you begin a public service job, use the PSLF Help Tool on studentaid.gov to confirm your employer qualifies.

- Submit Employment Certification Form (ECF) Annually: Even if you haven’t made 120 payments yet, submit the ECF each year or whenever you change employers. This ensures your payments are being counted correctly from the start.

- Enroll in an IDR Plan: To qualify for PSLF, you must be on an eligible income-driven repayment plan. The enhanced IDR plan discussed above is a perfect complement.

- Keep Meticulous Records: While tracking is improving, always keep copies of your ECFs, payment confirmations, and employment history.

Program 3: The Graduate Student Loan Interest Deferment and Subsidy Initiative

While the previous programs primarily target undergraduate loans or broad repayment strategies, the third new initiative for 2026 graduates specifically addresses the often-higher balances and unique repayment challenges faced by graduate and professional students. This program focuses on alleviating the burden of interest accumulation, which can significantly inflate the total cost of a graduate degree.

Innovative Components:

- Automatic Interest Deferment During Qualifying Periods: For certain graduate programs (e.g., medical residencies, specific doctoral programs with mandatory unpaid or low-paid training), this initiative provides for automatic interest deferment. This means interest will not accrue on your federal graduate loans during these pre-defined periods, allowing you to focus on your training without the added stress of a ballooning loan balance. This is a crucial benefit for managing student loan repayment 2026, especially for those with extended training.

- Interest Rate Subsidy for Early Career Professionals: For a specified period (e.g., the first 1-3 years) after completing a graduate program and entering the workforce, the government will subsidize a portion of the interest on your federal graduate loans. This means you pay less in interest, and your payments go further in reducing your principal balance. This acts as a crucial buffer during the often-lean early years of a professional career, making student loan repayment 2026 more manageable.

- Expanded Grace Period for Graduate Loans: While federal loans typically have a 6-month grace period, this initiative may extend that period for graduate students, allowing more time to secure employment and stabilize finances before repayment begins. This additional breathing room can be invaluable for 2026 graduates transitioning from academia to their professional lives.

- Targeted Loan Counseling: As part of this initiative, graduate students will receive enhanced, specialized loan counseling focusing on the unique aspects of graduate loan repayment, including strategies for managing higher balances and understanding specific programs relevant to their professional fields.

Who Benefits Most?

This program is tailor-made for 2026 graduates pursuing advanced degrees – particularly those in fields requiring extensive post-graduate training, such as medicine, law, or research. It acknowledges the substantial investment in graduate education and aims to reduce the long-term financial strain associated with it. It directly tackles one of the biggest pain points for graduate borrowers: the relentless accumulation of interest. This makes student loan repayment 2026 significantly less daunting for this demographic.

Actionable Steps:

- Identify Eligible Programs: Check if your graduate program or post-graduate training falls under the qualifying criteria for automatic interest deferment.

- Understand Subsidy Terms: Familiarize yourself with the duration and percentage of the interest rate subsidy available to you in your early career.

- Engage in Enhanced Counseling: Take advantage of the specialized graduate loan counseling to fully understand your options and optimize your repayment strategy.

- Monitor Your Loan Statements: Ensure that interest deferment and subsidies are being applied correctly to your account once you become eligible.

Maximizing Your Strategy: Combining Programs for Optimal Student Loan Repayment 2026

While each of these new programs offers significant benefits on its own, the true power lies in understanding how they can be combined and leveraged to create a comprehensive, personalized student loan repayment 2026 strategy. For instance, a 2026 graduate pursuing a public service career after a graduate degree could potentially benefit from all three programs.

A Synergistic Approach:

- Enhanced IDR + PSLF: This is a classic powerful combination. By enrolling in the enhanced IDR plan, your monthly payments are significantly reduced, and interest accrual is subsidized. These lower, subsidized payments then count towards the 120 payments required for PSLF. This means you pay less out of pocket, and your loan balance doesn’t grow, all while you work towards complete forgiveness. This is the gold standard for student loan repayment 2026 for public servants.

- Graduate Deferment/Subsidy + Enhanced IDR: For graduate students not pursuing PSLF, the graduate interest deferment and subsidy initiative provides a strong start by preventing interest from accumulating during critical training periods and reducing it in early career. Once these specific benefits expire, transitioning to the enhanced IDR plan ensures your payments remain affordable based on your income, providing a long-term safety net.

- Strategic Planning from Day One: As a 2026 graduate, your repayment journey begins even before you make your first payment. Use your grace period wisely to research, apply for the most suitable programs, and set up your financial plan. Don’t wait until payments are due to explore your options.

It is crucial to remember that eligibility criteria and program specifics can evolve. Always refer to the official studentaid.gov website and communicate directly with your loan servicer for the most accurate and up-to-date information regarding student loan repayment 2026. Financial advisors specializing in student debt can also provide invaluable personalized guidance.

Beyond the Programs: Additional Strategies for Smart Student Loan Repayment 2026

While these new programs offer substantial relief, a holistic approach to student loan repayment 2026 involves more than just enrolling in the right plan. Here are additional strategies to consider:

Build an Emergency Fund:

Having 3-6 months of living expenses saved can provide a crucial buffer against unexpected financial hardships, preventing you from missing loan payments or incurring additional debt. This financial stability complements any repayment plan you choose.

Create a Detailed Budget:

Understanding where your money goes is fundamental to effective financial management. A budget helps you identify areas where you can save, allowing you to potentially make extra payments on your loans or build other savings.

Explore Employer Assistance Programs:

Some employers offer student loan repayment assistance as part of their benefits package. This could be a direct contribution to your principal or matching contributions. Always inquire about such programs during your job search or with your current employer.

Consider Refinancing Private Loans:

While federal loans offer robust protections and repayment options, private loans typically do not. If you have private student loans and a strong credit score, refinancing could secure a lower interest rate, reducing your total cost of borrowing. However, be cautious and understand that refinancing federal loans into private ones means losing federal protections like IDR and forgiveness programs.

Automate Payments:

Setting up automatic payments can prevent missed deadlines and sometimes even qualifies you for a small interest rate reduction (e.g., 0.25%). Consistency is key in student loan repayment 2026.

Understand Tax Implications:

Student loan interest deduction can offer tax relief. Additionally, understanding the tax implications of loan forgiveness (some forgiven amounts may be considered taxable income, though some federal forgiveness is currently tax-free) is important for long-term planning.

Conclusion: Empowering Your Financial Future as a 2026 Graduate

For the class of 2026, the journey into post-graduation life is filled with exciting possibilities, but also the very real challenge of student loan repayment. The introduction of these three new programs – the Enhanced Income-Driven Repayment Plan, the Public Service Loan Forgiveness Expansion, and the Graduate Student Loan Interest Deferment and Subsidy Initiative – represents a significant step towards making that journey more manageable and less financially burdensome. By proactively understanding and utilizing these resources, 2026 graduates have an unprecedented opportunity to take control of their student debt.

Remember, knowledge is power. Do not shy away from researching, asking questions, and seeking professional advice. Your financial future is a direct result of the decisions you make today. Embrace these new tools for student loan repayment 2026, combine them with smart financial habits, and pave your way to a future free from the overwhelming weight of student debt. The path to financial well-being after graduation starts now, with informed choices and strategic action.